Dax Function: DURATION

Reviewed by Neetu Singla — Founder, Lets Viz Technologies — AI & Data Consultant. Last reviewed June 5, 2026.

Reviewed by Neetu Singla — Founder, Lets Viz Technologies — AI & Data Consultant. Last reviewed June 5, 2026.Category: Financial Functions

The DURATION function calculates the Macaulay duration of a security that pays periodic interest. Macaulay duration is a weighted average time until the cash flows from a bond are received, and it’s widely used in bond valuation and interest rate risk analysis.

Purpose

To measure the sensitivity of a bond’s price to interest rate changes.

To help investors and analysts understand the average time it takes to recover the bond’s price through cash flows.

A vital tool for managing fixed-income portfolios and assessing interest rate risk.

Type of Calculations

Performs financial calculations to determine the weighted average time until a bond’s cash flows are received.

Takes into account factors like coupon payments, yield, and time to maturity.

Practical Use Cases

Portfolio Duration Matching: Aligning portfolio durations with liabilities to hedge against interest rate changes.

Bond Analysis: Evaluate the interest rate risk associated with different securities.

Investment Strategy: Optimize fixed-income allocations by understanding cash flow timing.

DURATION(settlement, maturity, coupon, yield, frequency, [basis])

| Parameter | Type | Description |

|---|---|---|

settlement | Scalar | The settlement date of the bond (date of purchase). |

maturity | Scalar | The maturity date of the bond (date of repayment). |

coupon | Scalar | The annual coupon rate (interest rate) as a percentage. |

yield | Scalar | The annual yield of the bond as a percentage. |

frequency | Scalar | Number of coupon payments per year: 1 = annual, 2 = semi-annual, 4 = quarterly. |

[basis] | Scalar | (Optional) Day count basis for the calculation. Default is 0. See day count conventions below: |

How Does DURATION Dax Function Works

Concept

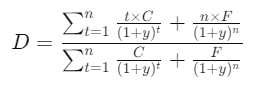

The Macaulay duration is calculated as:

Where:

C: Coupon payment

y: Yield per period

n: Number of periods to maturity

F: Face value

The function automates this formula, considering settlement date, maturity date, coupon rate, yield, and payment frequency.

What Does It Return?

Returns the Macaulay duration as a scalar value.

The result is typically expressed in years.

When Should We Use It?

Assess Bond Sensitivity: Evaluate how price changes relative to interest rate movements.

Portfolio Optimization: Determine the weighted average maturity of cash flows for fixed-income investments.

Compare Securities: Compare bonds with different maturities, coupons, and yields.

Examples

Basic Usage :

Calculate the Macaulay duration of a bond with the following details:

Settlement:

01/01/2023Maturity:

01/01/2030Coupon:

5%Yield:

4%Frequency:

2(semi-annual payments)

DURATION(DATE(2023,1,1), DATE(2030,1,1), 0.05, 0.04, 2)

Result: 6.45 years (approx.)

Column Usage

Apply DURATION to a table of bond details for portfolio analysis.

PortfolioDuration =

DURATION(

Table[SettlementDate],

Table[MaturityDate],

Table[CouponRate],

Table[YieldRate],

Table[Frequency]

)

Calculates the duration for each bond in the table.

Advanced Usage

Combine DURATION with other DAX functions to filter bonds based on duration.

FilteredDuration =

CALCULATE(

AVERAGEX(

FILTER(Bonds, DURATION(Settlement, Maturity, Coupon, Yield, Frequency) > 5),

DURATION(Settlement, Maturity, Coupon, Yield, Frequency)

)

)

Calculates the average duration of bonds with durations greater than 5 years.

Tips and Tricks

Use consistent date formats for

settlementandmaturityparameters to avoid errors.Ensure coupon and yield values are expressed as percentages (e.g., 5% as

0.05).Negative results: Ensure settlement date is before maturity.

Basis mismatch: Use the correct

basisfor your market or financial standard.

Performance Impact of DURATION DAX Function:

Large Datasets: Avoid applying

DURATIONto excessively large datasets row-by-row to optimize performance.Complex Formulas: Use intermediate calculations if working with highly detailed financial models.

Related Functions You Might Need

| Function | Description |

|---|---|

YIELD | Calculates the yield of a security that pays periodic interest. |

PRICE | Computes the price of a bond based on its yield, maturity, and coupon rate. |

PV | Calculates the present value of a series of cash flows. |

CUMPRINC | Determines cumulative principal payments for a loan or investment over a specified period. |

Want to Learn More?

For more information, check out the official Microsoft documentation for DURATION You can also experiment with this function in your Power BI reports to explore its capabilities.

Unlock the full capabilities of Power BI and elevate your data insights with our specialized consulting services. Whether you need guidance on advanced DAX functions like those highlighted here, support in designing interactive dashboards, or expertise in optimizing data models for enhanced performance, our experienced Power BI consultants are equipped to deliver customized solutions for your business. Explore our Power BI Consulting Services page to discover how we can help your organization make smarter, data-driven decisions.

The DURATION function calculates the Macaulay duration of a bond, measuring its price sensitivity to interest rate changes.

Yes, the DURATION function supports zero-coupon bonds by setting the coupon rate to 0.

The frequency parameter determines how often the bond pays interest (e.g., annual, semi-annual).

While DURATION measures interest rate sensitivity, YIELD calculates the rate of return on a bond based on its price and cash flows.

Need Power BI help in a real engagement?

Our team writes DAX like this every day for SaaS finance and ops teams. Refresh monitoring, change requests with a 2-business-day SLA, and a named analyst on retainer — or scoped hourly help if you just need a fix.

Named analyst2-day SLAFrom $5K/mo