GDPR Compliant SaaS Financial Reporting: The BI Checklist

GDPR compliant SaaS financial reporting means configuring your BI stack so that personal data embedded in financial records - subscriber names, invoice histories, usage-linked revenue - is processed lawfully, stored in approved jurisdictions, access-controlled at the row level, and fully auditable. Cross-border SaaS companies must also satisfy PIPEDA in Canada and, for US entities, align with SOC 2 Type II data-handling standards.

Key Takeaways

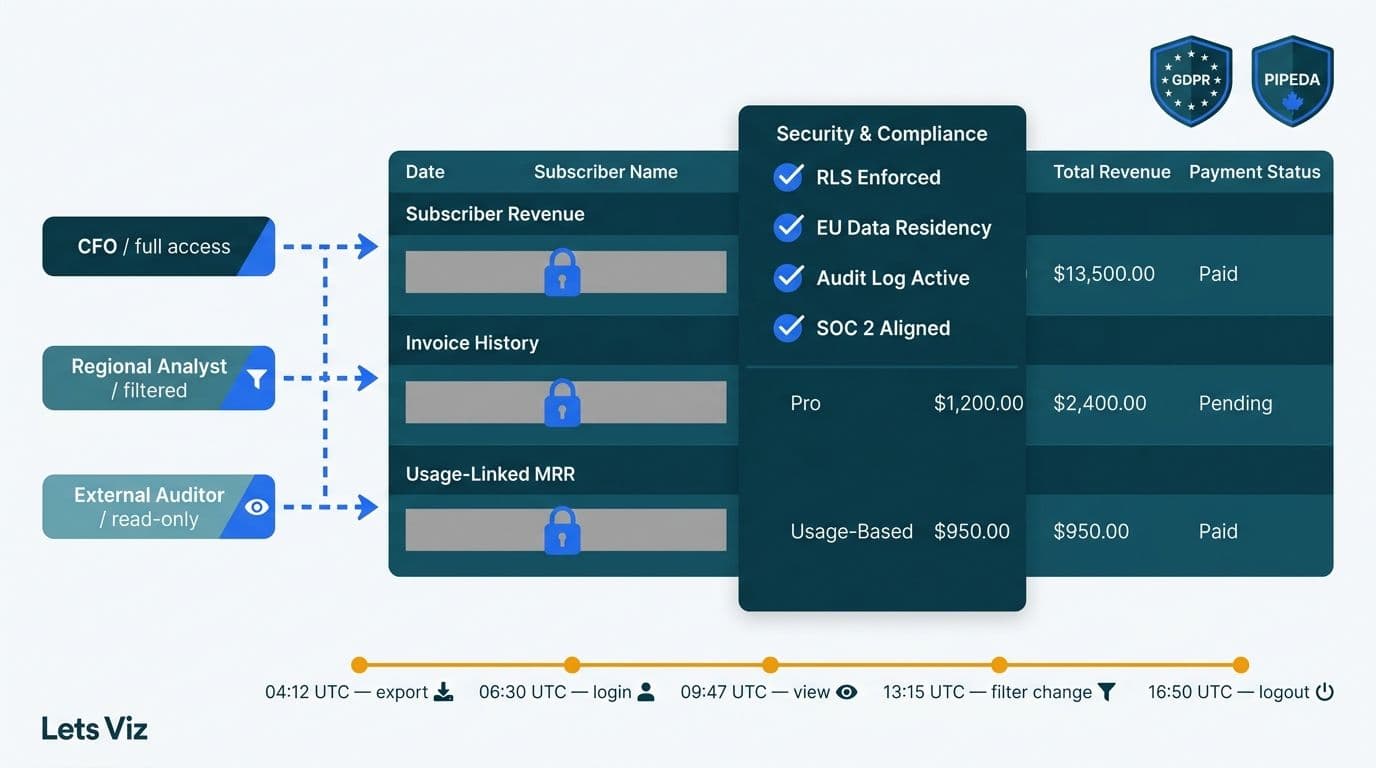

Row-level security (RLS) controls who sees which subscriber revenue records - without it, a shared financial report can expose personal data to unauthorized staff.

Data residency must be set at the workspace or capacity level before any financial data enters the cloud.

A documented audit trail is required under GDPR Article 30 and PIPEDA Principle 4.7, logging who queried what and when.

SaaS metrics for board reporting (ARR, Rule of 40, NRR) are safe when aggregated to cohort level - individual subscriber records must never be directly reachable from a board view.

Compliance is a configuration discipline, not a product purchase - every major BI platform needs the same deliberate hardening.

What Does GDPR Compliant SaaS Financial Reporting Actually Require?

GDPR Article 5(1)(f) requires personal data be processed with "appropriate technical and organisational measures." In a BI stack, that means workspace permissions, encrypted pipelines, role-based access controls, and documented retention policies. For SaaS companies, financial data almost always contains personal data: customer names tied to ARR, email addresses in invoice exports, or device IDs linked to usage revenue. Each creates a GDPR obligation the moment it leaves your transactional system and enters a reporting layer.

The critical distinction regulators draw is between aggregated metrics - a $42M ARR cohort view carries no GDPR risk - and granular subscriber-level data, which is personal data in scope regardless of how the column is labelled. The Power BI for SaaS finance teams practice covers how to build data models that segregate these two layers from the ground up, so the analytical foundation is compliant before the first report is published.

Industry analysis cited by Yahoo Finance (2026) projects AI consulting and support services to grow at a 31.6% CAGR through 2030 — a trajectory already accelerating as GDPR enforcement actions and comparable regulatory frameworks drive sustained compliance spend across SaaS finance and beyond.

How Does Row-Level Security Enforce GDPR Data Minimization?

Row-level security (RLS) ensures a regional finance director in Frankfurt sees only DACH subscriber revenue while the CFO in New York sees the global view - same report, same dataset, with access enforced at query time by the BI engine rather than by user discipline.

In Power BI, RLS uses DAX filter expressions defined at the dataset level. For cross-segment analysis where a controller needs rolled-up totals without touching raw subscriber rows, the DAX CROSSFILTER function governs which table relationships are active in a given calculation context, preventing granular records from leaking through aggregation measures. The DAX SUMMARIZE vs SUMMARIZECOLUMNS finance reporting guide covers how these functions interact when building revenue summaries that must stay compliant under drill-down.

A UK fintech SaaS company under UK GDPR - supervised by the ICO post-Brexit - would configure RLS so its London FP&A analyst sees payment cohort data but never individual transaction records tied to identifiable customers. This satisfies both the data minimization principle (Article 5(1)(c)) and internal need-to-know controls in a single dataset-level configuration.

RLS implementation checklist:

Define roles at the dataset level before publishing - report-level filters can be bypassed by users; dataset-level RLS cannot

Test each role via 'View as role' in Power BI Desktop, impersonating a sample user from every role before publishing

Map roles to Azure AD security groups, not individual users, so offboarding removes access automatically

Document every role definition in your GDPR Article 30 records of processing activities

What Are the Data Residency Options for EU and Cross-Border SaaS Reporting?

Under GDPR Article 46, personal data cannot leave the EEA unless the destination country holds an adequacy decision or Standard Contractual Clauses (SCCs) are in place. In Power BI and Microsoft Fabric, residency is set at the Premium capacity or Fabric capacity level - not per dataset. This architectural decision must be made before data ingestion; it cannot be retrofitted after subscriber financial data has already entered a workspace in the wrong geography.

| Region | Applicable Law | Power BI / Fabric Region | Transfer Mechanism Needed? |

|---|---|---|---|

| EU (Germany, Ireland, Netherlands) | GDPR | West Europe / North Europe | None (within EEA) |

| UK | UK GDPR (ICO) | UK South / UK West | EU-UK adequacy decision in effect |

| Canada | PIPEDA | Canada Central / Canada East | EU-Canada adequacy decision in effect |

| United States | SOC 2 / state privacy laws | East US / West US | SCCs required, or EU-US Data Privacy Framework (DPF) for certified entities |

A Canadian SaaS platform - for example, a Toronto-based subscription analytics company serving EU enterprise clients - must choose between operating separate capacities per jurisdiction or an architecture where EU subscriber data never leaves an EEA-region capacity. PIPEDA Principle 4.6 requires protection "regardless of the country in which it is processed," meaning cross-border transfers within one workspace still need documented contractual safeguards.

For US-headquartered SaaS companies with EU subscribers, the common solution is a dedicated EU capacity for EU subscriber financial data, with aggregated non-personal metrics replicated to a US workspace for global board reporting. Companies certified under the EU-US Data Privacy Framework (DPF) — in effect since July 2023 and reaffirmed through 2026 Commission reviews — can transfer EU subscriber financial data without SCCs, provided the DPF self-certification explicitly covers the relevant data categories; uncertified US entities still require SCCs. Using DirectQuery into a residency-compliant data warehouse avoids importing personal data into the BI layer at all - an approach explored in the Power BI Import vs DirectQuery mid-market decision guide.

How to Build an Audit Trail That Satisfies GDPR Article 30 and PIPEDA

An audit trail in a BI context is a timestamped log of who accessed which report, which dataset was queried, and what exports were made. GDPR Article 30 requires records of processing activities; PIPEDA Principle 4.7 requires safeguards against "unauthorized access, disclosure, copying, use or modification." Both regulators increasingly treat BI access logs as front-line evidence in enforcement reviews.

Minimum requirements for a compliant SaaS BI stack:

1. Activity log export - Power BI's audit log via Microsoft Purview or the Admin REST API captures every report view, dataset refresh, and export event. Export to a SIEM or data lake on a daily schedule.

2. Retention alignment - Match log retention to your GDPR or PIPEDA data retention schedule. UK and EU tax rules typically require seven-year financial record retention; audit logs covering that data should be kept for the same period.

3. Export controls - Log and alert on any CSV or Excel export from reports containing personal financial data. GDPR Article 32 requires demonstrating exports were authorized and necessary.

4. Named user access only - Shared service-account credentials break the audit chain and are indefensible in a supervisory authority review. Review service account access quarterly.

5. Breach detection trigger - Alert on anomalous export volumes or access from unexpected geographies. GDPR Article 33 requires notifying the supervisory authority within 72 hours of discovering a personal data breach.

Market Research Future (2025) projects the healthcare financial analytics market to grow at an 8.58% CAGR through 2035, driven significantly by regulatory compliance requirements - a trend equally visible in SaaS finance teams building audit-ready BI environments. The AI analytics data privacy risks and audit guide details analogous logging controls that transfer directly to financial data governance.

SaaS Metrics for Board Reporting: What to Anonymise and What You Can Show

SaaS metrics for board reporting - ARR, MRR, Net Revenue Retention, Gross Revenue Retention, and the Rule of 40 SaaS benchmark (revenue growth rate plus EBITDA margin; a result of 40 or above signals a healthy SaaS business by most investor standards) - are aggregated performance indicators. Used at cohort or company level they carry no personal data and no GDPR risk.

Compliance exposure appears in three common board reporting patterns:

Customer-level ARR waterfalls showing named enterprise accounts - even in B2B SaaS, a named contact tied to an account constitutes personal data under GDPR

Churn analysis by segment where individual customer metadata sits in the underlying dataset and is accessible via drill-through even when the surface view appears anonymized

CAC and LTV drill-throughs that allow a board member or analyst to click from an aggregate metric into subscriber-level rows

The safest architecture separates a presentation layer (pre-aggregated measures and anonymized cohorts built for board consumption) from an analytical layer (granular data with RLS applied, accessible only to named finance staff with documented GDPR justification). One overlooked gap for US SaaS companies: a board deck exported as a PDF containing named enterprise customer revenue becomes a GDPR-regulated document the moment it lands in an EU-based board member's inbox. The risk is not only inside the dashboard - it extends to every downstream artifact the dashboard generates.

GDPR vs PIPEDA vs SOC 2: What Each Framework Demands from Your BI Stack

Building to GDPR standard typically brings a deployment within scope for PIPEDA and SOC 2 data-handling requirements simultaneously - the incremental work is documentation. PIPEDA requires a designated privacy officer; SOC 2 requires independent auditor attestation.

| Control Area | GDPR (EU/UK) | PIPEDA (Canada) | SOC 2 Type II (US) |

|---|---|---|---|

| Legal basis for processing | Required; document in Art. 30 record | Consent or legitimate business purpose | Not mandated; policy-driven |

| Data residency | Must stay in EEA or adequate country | Must stay in Canada or have contractual safeguards | No geographic mandate |

| Row-level security | Mandatory - data minimization Art. 5 | Mandatory - Principle 7 | CC6.1 logical access controls |

| Audit logging | Art. 30 records and Art. 32 security | Principle 4.7 safeguards | CC7.2 system monitoring |

| Retention limits | Purpose-specific; right to erasure Art. 17 | Purpose-specific; Principle 5 | Policy-defined |

| Breach notification | 72 hours to supervisory authority | PIPEDA BENS; significant risk threshold | Per service agreement |

| Data subject rights in BI | Right to access and erasure applies | Limited right of access | Not mandated |

For a multi-jurisdiction SaaS company - a US-headquartered analytics platform with a UK subsidiary and Canadian enterprise clients - this table is the configuration checklist. GDPR is the most demanding on technical controls; meeting it sets the floor for the other two frameworks.

When Should You Engage a GDPR Financial Reporting Consultant?

The full configuration work - RLS design, workspace architecture, audit log pipeline, retention policy, and Article 30 records - typically takes a qualified Power BI architect two to four weeks for a mid-market SaaS company. The most common trigger for outside engagement is a DPO or legal review surfacing gaps just before an EU enterprise contract closes, or an ICO inquiry requiring documentation that was never built.

SaaS financial reporting consultant cost by engagement type:

Full implementation (RLS, residency, audit pipeline, documentation): USD 8,000 to USD 25,000 for a mid-market SaaS company

Existing environment audit with remediation report: USD 2,000 to USD 6,000

These ranges assume a specialist combining Power BI architecture expertise with data privacy knowledge - a pairing that remains scarce relative to demand. According to Future Market Insights (2026), the AI consulting services market — valued at approximately USD 14 billion as of 2026 — is on track to reach USD 90.99 billion by 2035, reflecting a sustained 26.2% CAGR that underscores how rapidly organizations are investing in expert-led, governed analytics buildouts. For teams assessing their current exposure before committing to a build, the free BI readiness assessment surfaces the most common GDPR gaps in an existing Power BI environment in under fifteen minutes.

---

About Lets Viz: Lets Viz has delivered governed analytics and compliant reporting solutions to SaaS finance teams, US healthcare organizations, UK fintech firms, and Canadian manufacturing companies since 2020, earning a 5.0 rating on Clutch. Our Power BI practice combines data architecture expertise with direct experience navigating GDPR, PIPEDA, and SOC 2 audit requirements across all three major geographies we serve.

If your SaaS reporting stack needs a GDPR compliance review or a ground-up build, Power BI for SaaS finance teams is where we start.